Africa in brief

World Bank criticises Kenya's approach

The World Bank urged Kenya to cut spending on public sector wages and other recurring items to reduce its debt load, instead of slashing development spending as that is restraining economic growth.

In a bi-annual economic update on the country, released on Thursday, the bank raised its estimate for Kenya’s 2018 economic growth to 5.7%, from a previous forecast of 5.5%.

While that would be faster than a 4.9% expansion in 2017, the Washington-based lender said Kenya was growing below its potential, likening it to a car driving at only 60 kilometres (37 miles) an hour.

“Kenya can be a Ferrari doing 150 kilometres per hour but it has to do certain things,” said Allen Dennis, the World Bank’s senior economist for Kenya.

Kenya’s total debt stands at 57% of GDP, the bank said, barely down from 57.5% a year ago.

Under pressure from the International Monetary Fund, the Kenyan government reduced its fiscal deficit by two percentage points in the financial year that ended in June, to 7% of gross domestic product, and has set a target of 5.8% of GDP this fiscal year.

-Nampa/Reuters

South Africa gets US$35 bln in investment pledges

South Africa has investment commitments of US$35 billion as part of plans by President Cyril Ramaphosa to attract US$100 billion over the next five years to revive the country’s flagging economy, his economic adviser told Reuters on Wednesday.

Ramaphosa has appointed a team of investment envoys - bankers, former ministers, business people as well as economist Trudi Makhaya, his economic adviser - to scour the world’s financial capitals for new investors.

“There is about US$35 billion that has been pledged,” Makhaya said. “We’ve had US$10 billion committed from Saudi Arabia. About US$10 billion from the UAE, and around US$15 billion committed from China when you’re looking at government to government deals.”

-Nampa/Reuters

Foreign holdings of Egyptian treasuries at US$14 bln

Foreign holdings of Egyptian treasuries stood at US$14 billion at the end of September, Deputy Finance Minister Ahmed Kouchouk was cited as saying on Thursday, a decline of nearly 20% from the end of June, according to Reuters calculations.

Holdings stood at US$17.5 billion at the end of June. Appetite for emerging market debt had already weakened when it declined further following currency crises in Turkey and Argentina in August. These triggered an exodus of foreign investors from Egypt who must also be repaid.

Kouchouk’s remarks were published in the online newsletter Enterprise.

The government cancelled four consecutive local currency T-bond auctions last month after bankers and investors demanded high yields on the debt.

-Nampa/Reuters

Sudan's annual inflation climbs to 68%

Sudan’s inflation edged up to 68.64% in September year-on-year, from 66.82% in August, the state statistics agency said on Thursday.

Inflation jumped to more than 50% in January, when subsidy cuts triggered food price increases that kindled unrest. Since then inflation has continued to accelerates steadily despite attempts to slow price rises with strict limits on cash withdrawals.

-Nampa/Reuters

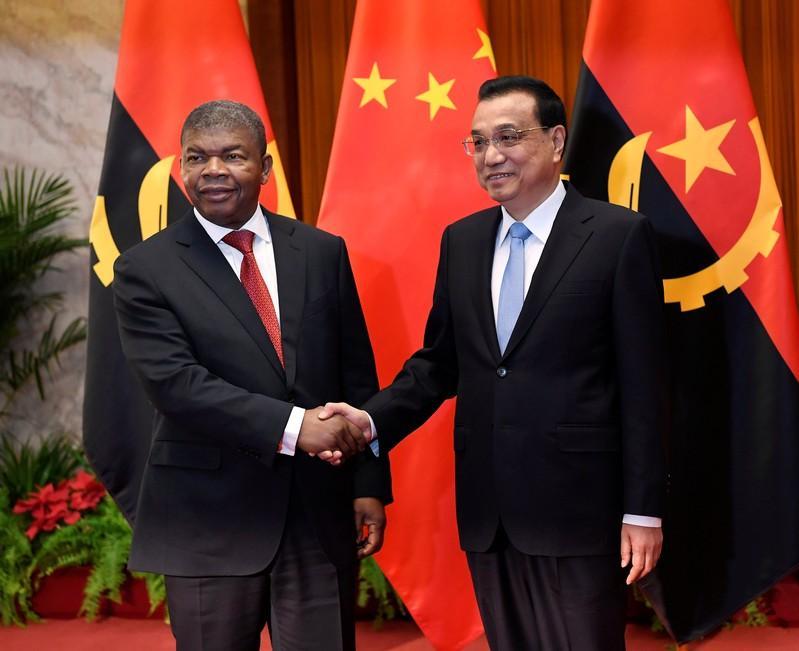

Angola secures US$2 bln in financing from China

Angola has secured US$2 billion in Chinese financing from the China Development Bank for infrastructure projects on President João Lourenço’s first visit to Beijing, Angola’s state newspaper Jornal de Angola reported on Wednesday.

Details of the terms of the financing were not released. The finance ministry did not immediately respond to a request to confirm the information.

China is increasingly flexing its financial muscle in Africa, funding massive infrastructure projects across the continent.

Angola, Africa’s second largest oil producer, is in the process of trying to diversify its economy since a fall in the price of crude in 2014 plunged it into recession. Inflation is running at more than 20% per year and at least one in five of workers are jobless.

Lourenço, who took power a year ago after the 38-year rule of Jose Eduardo dos Santos, has promised to oversee an “economic miracle” by opening up the country to foreign investment and prioritising sectors such as agriculture and tourism. So far growth has remained sluggish.

-Nampa/Reuters

The World Bank urged Kenya to cut spending on public sector wages and other recurring items to reduce its debt load, instead of slashing development spending as that is restraining economic growth.

In a bi-annual economic update on the country, released on Thursday, the bank raised its estimate for Kenya’s 2018 economic growth to 5.7%, from a previous forecast of 5.5%.

While that would be faster than a 4.9% expansion in 2017, the Washington-based lender said Kenya was growing below its potential, likening it to a car driving at only 60 kilometres (37 miles) an hour.

“Kenya can be a Ferrari doing 150 kilometres per hour but it has to do certain things,” said Allen Dennis, the World Bank’s senior economist for Kenya.

Kenya’s total debt stands at 57% of GDP, the bank said, barely down from 57.5% a year ago.

Under pressure from the International Monetary Fund, the Kenyan government reduced its fiscal deficit by two percentage points in the financial year that ended in June, to 7% of gross domestic product, and has set a target of 5.8% of GDP this fiscal year.

-Nampa/Reuters

South Africa gets US$35 bln in investment pledges

South Africa has investment commitments of US$35 billion as part of plans by President Cyril Ramaphosa to attract US$100 billion over the next five years to revive the country’s flagging economy, his economic adviser told Reuters on Wednesday.

Ramaphosa has appointed a team of investment envoys - bankers, former ministers, business people as well as economist Trudi Makhaya, his economic adviser - to scour the world’s financial capitals for new investors.

“There is about US$35 billion that has been pledged,” Makhaya said. “We’ve had US$10 billion committed from Saudi Arabia. About US$10 billion from the UAE, and around US$15 billion committed from China when you’re looking at government to government deals.”

-Nampa/Reuters

Foreign holdings of Egyptian treasuries at US$14 bln

Foreign holdings of Egyptian treasuries stood at US$14 billion at the end of September, Deputy Finance Minister Ahmed Kouchouk was cited as saying on Thursday, a decline of nearly 20% from the end of June, according to Reuters calculations.

Holdings stood at US$17.5 billion at the end of June. Appetite for emerging market debt had already weakened when it declined further following currency crises in Turkey and Argentina in August. These triggered an exodus of foreign investors from Egypt who must also be repaid.

Kouchouk’s remarks were published in the online newsletter Enterprise.

The government cancelled four consecutive local currency T-bond auctions last month after bankers and investors demanded high yields on the debt.

-Nampa/Reuters

Sudan's annual inflation climbs to 68%

Sudan’s inflation edged up to 68.64% in September year-on-year, from 66.82% in August, the state statistics agency said on Thursday.

Inflation jumped to more than 50% in January, when subsidy cuts triggered food price increases that kindled unrest. Since then inflation has continued to accelerates steadily despite attempts to slow price rises with strict limits on cash withdrawals.

-Nampa/Reuters

Angola secures US$2 bln in financing from China

Angola has secured US$2 billion in Chinese financing from the China Development Bank for infrastructure projects on President João Lourenço’s first visit to Beijing, Angola’s state newspaper Jornal de Angola reported on Wednesday.

Details of the terms of the financing were not released. The finance ministry did not immediately respond to a request to confirm the information.

China is increasingly flexing its financial muscle in Africa, funding massive infrastructure projects across the continent.

Angola, Africa’s second largest oil producer, is in the process of trying to diversify its economy since a fall in the price of crude in 2014 plunged it into recession. Inflation is running at more than 20% per year and at least one in five of workers are jobless.

Lourenço, who took power a year ago after the 38-year rule of Jose Eduardo dos Santos, has promised to oversee an “economic miracle” by opening up the country to foreign investment and prioritising sectors such as agriculture and tourism. So far growth has remained sluggish.

-Nampa/Reuters

Comments

Namibian Sun

No comments have been left on this article